The grain market remains under pressure. While the front month of March 2024 was still trading at 208.50 euros/t at the closing bell last Friday, it was still 206.00 euros/t yesterday evening. The losses were significant in the now most traded May contract, which fell from 206 euros/t to 199.75 euros/t. Corn also trended weaker this week and cost 173.75 euros/t in the most traded June contract yesterday evening; a week ago it was still 178.75 euros/t in the contract on the Euronext/Matif display board. A similar picture emerges at the CBoT. At the beginning of the week, the WASDE from last Thursday was still having an impact. The slightly increased global production caused wheat production to decline. The International Grain Council also issued a new global production forecast this week and expects a wheat harvest of 788 million tonnes. The IGC forecast is therefore slightly higher than that of the USDA, but both expect a slightly smaller harvest than last year. The high price competition from the Black Sea continues to put price pressure on the European and American grain markets. In a tender from Egypt, suppliers from Romania were also able to prevail, but it is said that the majority of deliveries come from Ukraine. It was already clear last week that Ukraine's exports picked up significantly, especially in December and January. No official information has been given about the extent of the damage when Russia attacked the port of Odessa with drones. In an initial estimate at the USDA's AG Outlook Forum yesterday, Thursday, the ministry's analysts announced a smaller acreage for the coming 2024/25 harvest, but producers are increasingly offering goods on the local cash markets following the recent price declines. Many market participants currently lack the imagination for rising prices as the season progresses. The feed industry in particular continues to demand in the long term. Corn prices are being weighed down by the good global supply situation. The advancing harvest in Brazil and good yield prospects for Argentina are also weighing on trade. As with wheat, the USDA expects a higher corn harvest for the coming harvest due to better yields.

Due to technical problems, the EU Commission has not published updated export and import data from customs statistics since the beginning of February.

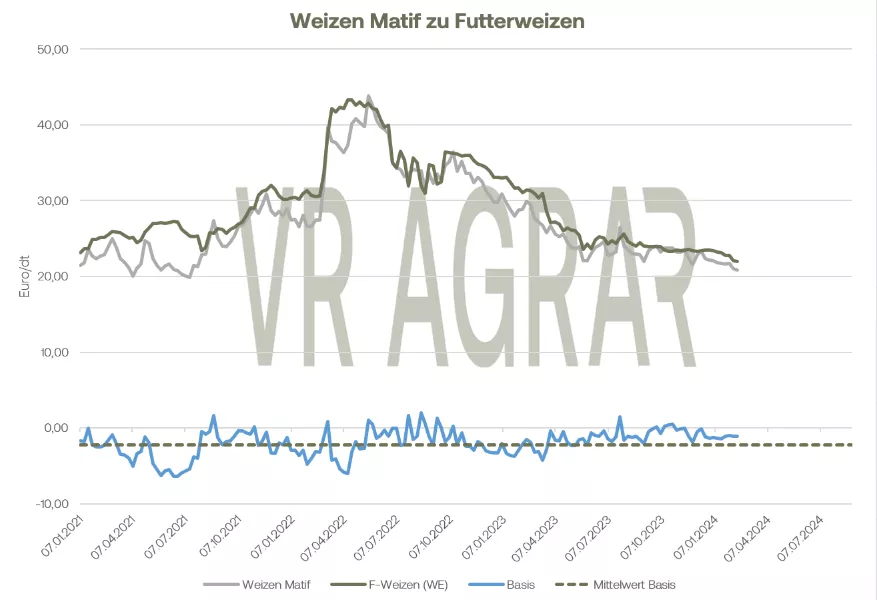

ZMP Live Expert Opinion

The overall grain supply is good and since Ukraine and Russia are able to deliver, international competition remains strong. Producers in this country are also experiencing slight pressure to sell, while the industry is taking a cautious approach in view of the current price development.