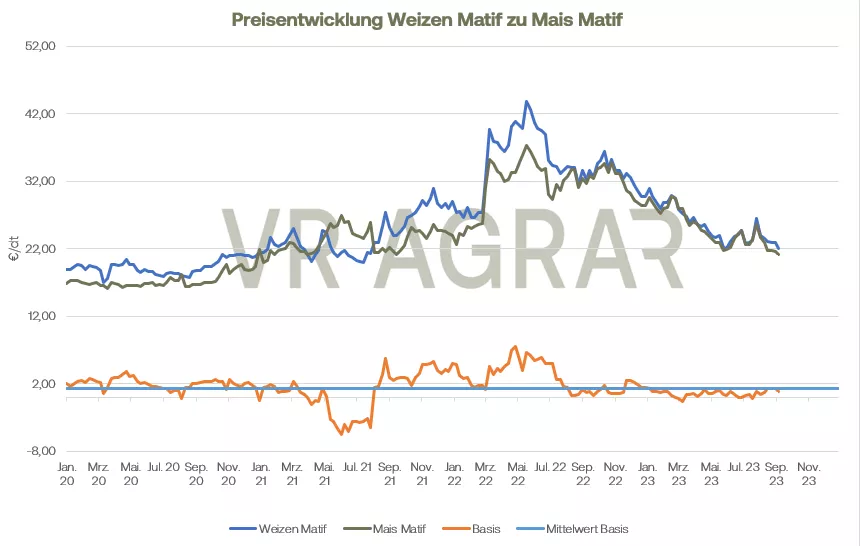

Wheat on Euronext/Matif rose over the course of the week. While the most traded December date was still at 235.00 euros last Friday, at the closing bell yesterday it was 238.50 euros/t. Maize was hardly changed this week and closed yesterday at a price of 214.00 euros/t in the front month of November, last week Friday it was still 212.50 euros/t. Many had pinned their hopes on a new grain agreement. Turkish President Erdogan traveled to Russia to explore the opportunities with his counterpart Putin. As expected, Russia has shown no interest in facilitating the Ukrainian transports. Instead, a deal has emerged whereby Russia will ship 1 million tons of wheat to Turkey for onward delivery to mainly African countries. Russia still sees its demands for trade facilitation not being met. As Erdogan announced, he is trying to find a solution in further talks with UN representatives. Meanwhile, Russia has attacked several ports in Ukraine, not targeting ports on the Danube, which are important for intra-European transport.In addition to geopolitical tensions, higher production prospects for Russia also played a role on the international markets. For Australia, however, the agricultural authority there has revised the production forecast downwards by 800,000 tons and is now expecting a harvest of 25.4 million tons of wheat in the 2023/24 marketing year. In the USA, the winter wheat harvest is now complete. The spring wheat harvest is in full swing, boosted by dry weather conditions in the Great Plains and northern growing regions. As of September 5, 74 percent of spring wheat stocks had been harvested. This is slightly slower than the average for the last five years, but faster than last year. Wheat shipments and wheat demand in the USA continue to be weak. Europe has also recently been able to export less wheat to third countries than in the same period last year. Local farmers remain largely satisfied with the development of the maize plants, but there are exceptions locally. The US condition assessment of corn stocks was revised downwards, as many market participants expected. Currently 53 percent of the stocks are classified as good or very good, compared to 56 percent last week.There are few changes on the local cash markets. Concentrated feed plants are still only sporadically looking for feed grain. However, the prices tend to be a little higher.

ZMP Live Expert Opinion

The harvest pressure on the market is slowly waning. Traders are already concentrating more and more on the prospects for the remaining half of the year and the production prospects in the southern hemisphere. The corn harvest in Europe and the USA is about to begin. The US stocks have recently suffered from heat and a lack of rainfall, while the northern European stocks have experienced plenty of rainfall. Overall, however, the European corn harvest is unlikely to be as high as was expected at the beginning of the year.