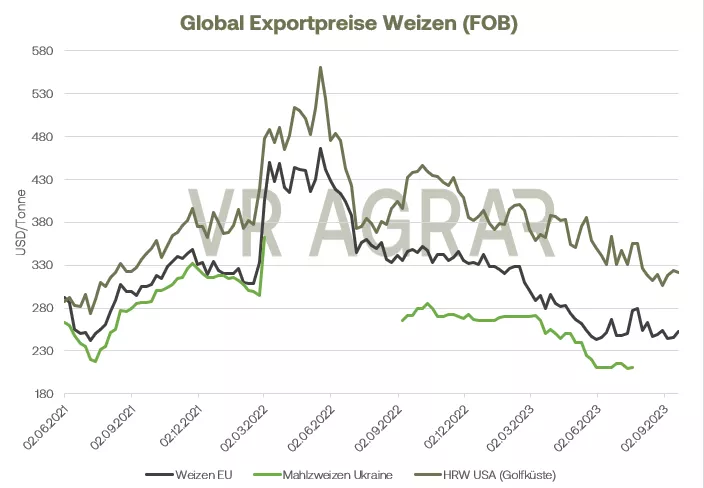

The grain markets were volatile this week. Compared to last Friday's closing price, wheat prices on Euronext/Matif fell until the closing bell on Thursday. The December date closed yesterday with a trading day price of 236.25 euros/t. Corn is also trading weaker and higher, from 213 euros on Friday to 208.25 uro/t yesterday, Thursday. A similar picture emerges when it comes to price developments overseas. The news situation has recently been just as diverse as the price development. In particular, the focus was on international export markets such as the situation in Ukraine. For the latter, the European storage ban in the countries neighboring Ukraine came to an end at the weekend. After Poland and Hungary announced national unilateral measures to maintain the storage ban, Ukraine initially responded by threatening to file a lawsuit with the World Trade Organization. However, yesterday it became known that the affected countries wanted to reach an agreement with Ukraine and that Ukraine, for its part, would present a compromise for the transit of its agricultural goods. A first ship made the journey to and from Ukraine after the end of the grain deal. The freighter is currently heading to Israel and, according to Ukraine, has 3.000 tons of wheat loaded. Agencies also reported that a freighter is currently being loaded with 20,000 tons of wheat in the port of Choromsorsk (Ukraine). Various purchase reports also provided temporary support for prices. Egypt is said to have bought around 120,000 tons of common wheat from Romania, and Algeria was also looking for wheat on the world market with a tender this week. However, European exports last week, at around 190,000 tonnes, were significantly below the values of the previous weeks. In total, Europe's exporters were able to export 6.3 million tons of common wheat by the 12th calendar week of the current marketing year. At this point in the previous year it was already 8.69 million tonnes. It therefore remains to be seen whether the EU Commission's forecast, which expects 32 million tons of common wheat exports, can be achieved. The recent development of the euro-US dollar currency pair is at least leading to better competitiveness for local exporters. The US export reports, however, were disappointing. Last week only 307,000 tons of US wheat were booked, which was another 130,000 tons less than a week earlier. The International Grain Council yesterday announced its forecast for the global wheat crop at 600.000 tons reduced compared to the last estimate. However, due to lower consumption expectations, ending stocks were noticeably increased. The forecast for corn is similar. Here, both production forecasts and global ending stocks are increasing in the latest estimate. As with wheat, corn demand in the US also disappointed this week. The advancing harvest and higher yield forecasts for Ukraine and Russia are also having a negative impact here. The APK-Inform analysis estimates that 15.6 million tons of corn will be harvested in Ukraine; previously the house had expected 14.8 million tons of corn. Overall, prices on the local cash markets were under pressure. Dutch buyers are currently primarily active in southern Germany and buy feed wheat here. Domestic concentrate feed factories are only cautiously active on the market. Overall, however, producers' sales pressure on feed wheat has decreased. Harvest volumes are currently putting less pressure on the market than they did a week or two ago. The corn harvest is currently beginning in many regions and is picking up speed. However, trade in grains is still subdued.

ZMP Live Expert Opinion

There is still no calm on the grain markets. Harvesting continues in the northern hemisphere. Russia's export prices are depressing the mood for wheat and the beginning of the corn harvest in Europe and the USA is causing price pressure in this submarket. At the same time, there are always questions about the global supply situation. Even if Ukraine can load ships and guide them safely through the Black Sea, the country's export capacity is fragile despite a good harvest.